WHAT WE DO

Learn about Namaste’s signature Creating Prosperity Program (CPP) and additional women’s economic empowerment services.

DONATE

Your investment will support women entrepreneurs to grow sustainable businesses, achieve financial security, and pursue their dreams.

ABOUT US

Our Team, Annual Reports, Impact, Strategic Plan, and Our Story.

our mission

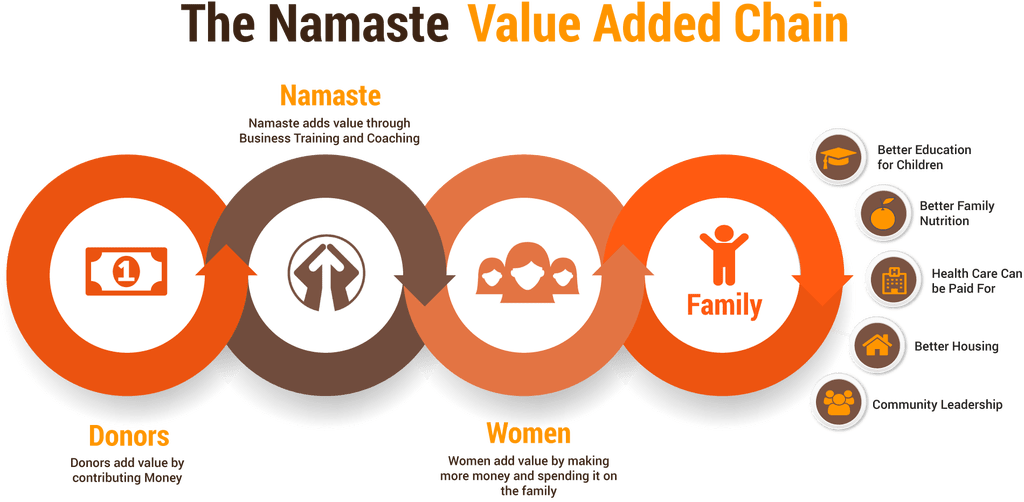

Namaste Direct is a nonprofit organization that is laser-focused on economically empowering women entrepreneurs in Guatemala to grow profitable businesses and lift themselves out of poverty.

Why? There is an overwhelming correlation between poverty and gender inequality. When women have the resources and opportunity to make and manage their money, they gain agency over their lives, invest in the well-being of their families, strengthen their communities, and make an immense contribution to the economy.

- 60% of the population lives in poverty in Guatemala.

- Guatemala has the 3rd highest rate of violent deaths for women in the world.

- There are very few traditional employment opportunities, especially for women.

- Over 70% of working women in Guatemala are self-employed in the informal workforce.

With an average of just four years of education, most women entrepreneurs lack financial literacy and basic business skills to run successful businesses.

Namaste’s mission is to empower economically vulnerable Guatemalan women with the skills and resources to grow profitable businesses, achieve financial security, and pursue their dreams.

Since 2008, Namaste has economically empowered 4,500 women through our signature Creating Prosperity Program (CPP). The CPP combines business advising, financial literacy training, and customized microloans to help women entrepreneurs formalize their business models, manage their finances, and dramatically increase their profits.

BUSINESS ADVISING

Business advisors are local community leaders, well versed in the local economy and also the indigenous language of the region.

FINANCIAL LITERACY

Each Namaste Entrepreneur learns important cash management techniques, such as separating business money from personal money.

CUSTOMIZED BUSINESS LOAN PROGRAM

Each woman’s business is unique, which is why the loans are tailored to the specific needs of each client.

TECHNOLOGY

The monitoring and evaluation system used by Namaste is based on a tailor made online database called PROSPER.

OUR VISION

Our vision is to reduce the incidence of poverty and gender inequality throughout Guatemala by equipping women entrepreneurs with the skills and resources they need to run profitable businesses, achieve financial independence and pursue their dreams.

María

Eva

Faustina

Lesbia

María Z.

Our Partners

Namaste celebrates 15 years of service to over 3,500 low-income micro-entrepreneurs, the top 70% of which more than doubled their monthly profits with our training!

NINE-MONTH TRAINING CYCLES

%

ATTENDANCE RATE

%

ADVICE IMPLEMENTED

WANT TO LEARN MORE ABOUT NAMASTE?

JOIN OUR EMAIL LIST AND RECIEVE QUARTERLY UPDATES!

meet the women you are helping

Silvia Isabel

Olga Marina

Romelia

Wanda